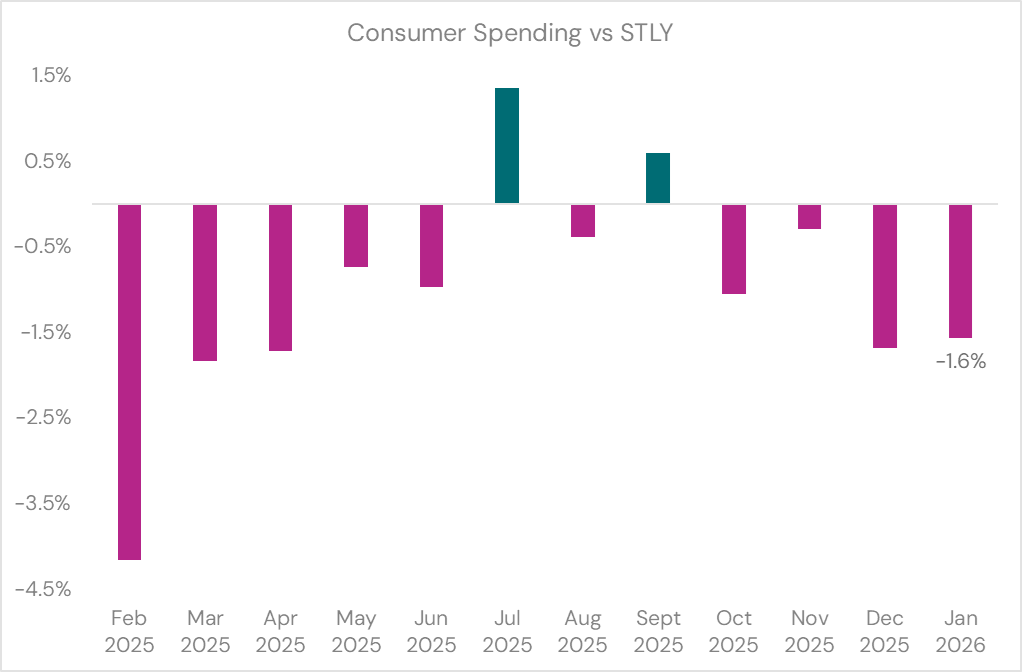

Twenty-twenty six kicked off with a -1.6% drop in spend from the same month last year. It’s a sea of red (or pink) when casting one’s eye over the last 12 months.

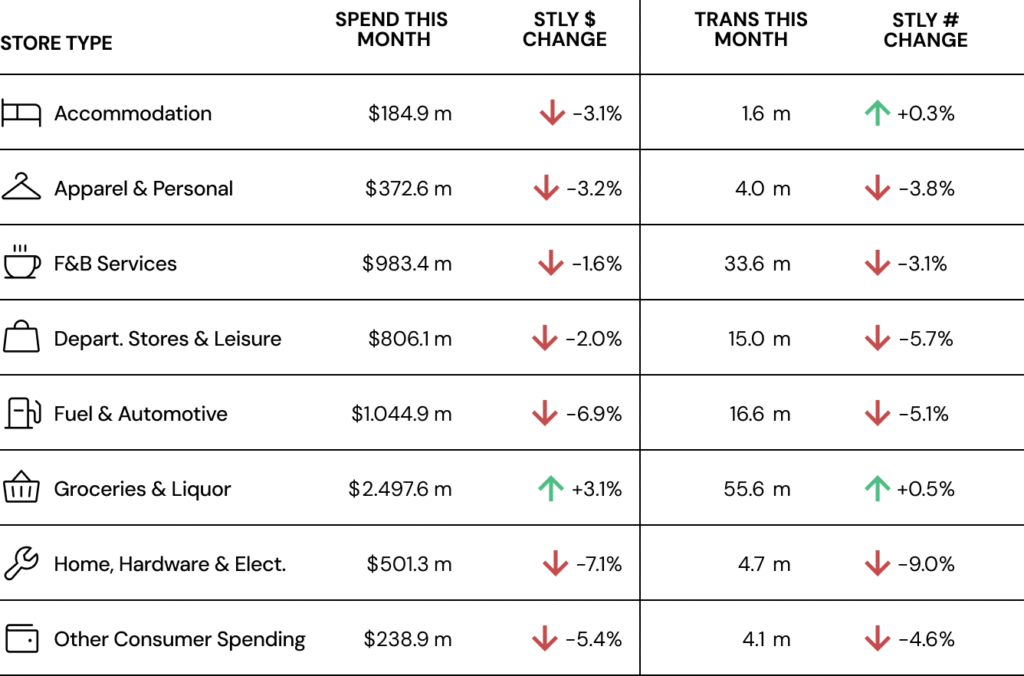

It’s a bit of a Groundhog Day with Groceries & Liquor leading the charge (+3.1%). All other storetypes were in the red. Again. Every transaction at the grocers’ and off licensees’ tills now average $44.90. What will that buy you at the supermarket these days?

New Zealanders are having a real hard time at the moment and collectively dropped spend by -2.1% from same month last year.

But this state of affairs is not homogenous throughout the country. Tasman cardholders continued to lift spend, up +3.5%. Northlanders joined them this month, up +0.1%. All other cardholders contracted spend.

Internationals, bless them (!), increased their spend by +5.5%, with Americans (+13.5%), Indians (+11.9%) and the Brits (+0.6%) driving spend.

Key insights for January 2026

- Consumer spending dropped -1.6% in January 2026, when compared to January 2025.

- Transactions dropped more, down -2.5%, showing a continued attempt to contain spend.

- Groceries & Liquor was the only storetype that saw growth this month, up +3.1%.

- Internationals increased spend by +5.5%. Key markets of growth include USA (+13.5%), India (+11.9), and UK (+0.6%).

- Domestics dropped spend by -2.1%. Of note are Tasman District and Northland cardholders who drove spend +3.5% and +0.1% respectively.

- A storetype breakdown is detailed in the table below: